it was a fairly busy week in the econo-blogosphere, accented by what should have been an uneventful monthly FOMC (Fed Open Market Committee) meeting & Bernanke press conference, that instead turned viral after an NY times reporter questioned Ben about an article penned by paul krugman earlier in the week under the headline “Earth to Ben Bernanke“; basically, krugman had asked why the Fed chairman wasnt following the monetary policy prescriptions he had recommended for Japan in a 2000 paper he authored as a professor at princeton (the back story is that bernanke had hired krugman at princeton, & both had written about Japan)…a number of economists & bloggers weighed in on both sides & tangentially, so if you’re interested, you can find the entire play by play at the beginning of this week’s global glass onion blogpost, right after the routine Fed coverage…

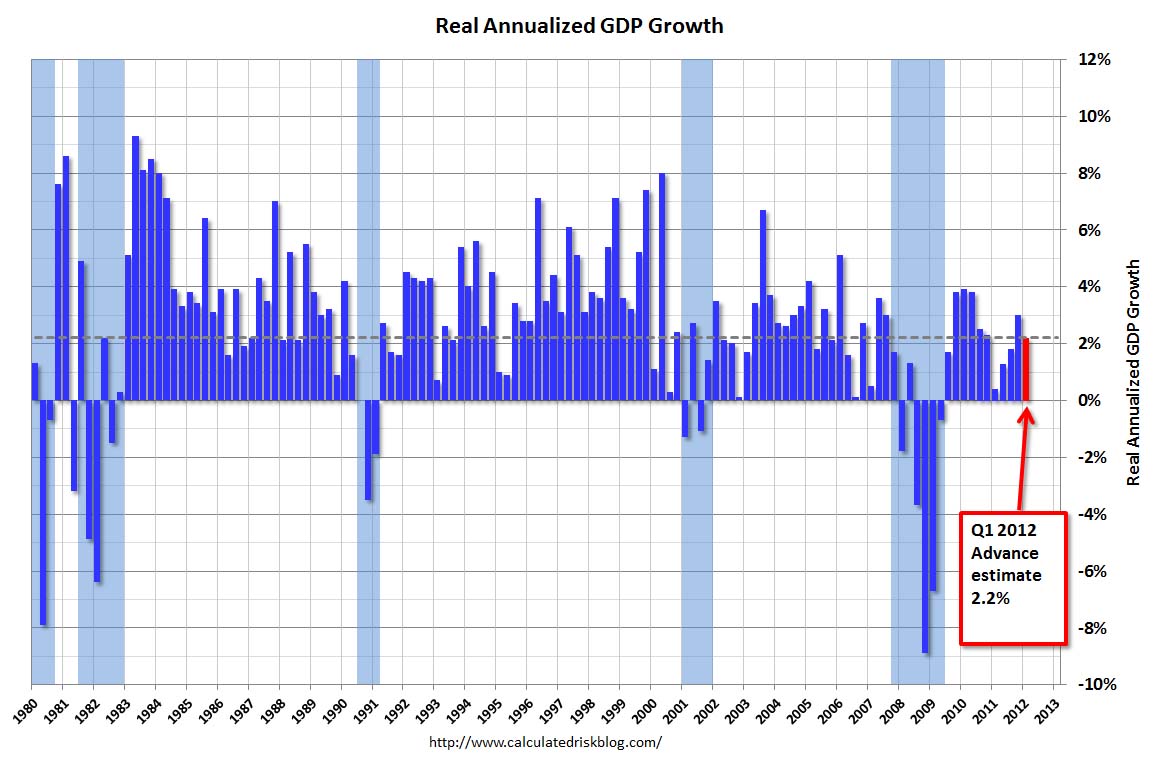

the major macroeconomic report out this week was the advance estimate of the 1st quarter GDP from the BEA; you may recall these quarterly reports are revised twice in the months following the first take, often by quite a bit, & then even later in annual revisions, but it’s the less accurate first estimate that garners all the headlines & analysis…at any rate, this initial report showed that the “real” gross domestic product — the country’s output of goods and services, adjusted by an inflation “deflator” — increased at an annual rate of 2.2% in the 1st quarter of this year; the bulk of the increase – about 90% of it – came from increased personal consumption expenditures (PCE); other major positive contributions came from increased private inventories and residential building, which were partly offset by declines in state, local & federal government spending, & nonresidential fixed investment…both imports & exports increased in the quarter, but the net effect of their changes on GDP was negligible…more than half of the PCE contribution came from purchases of durable goods (like cars & appliances); consumer services spending was weakened by decreased utility use in the warmest 1st quarter on record, and despite higher gas prices, spending for fuel subtracted from the quarter’s non-durable purchases, as we apparently continued to drive less…in the government sectors, federal spending & investment decreased 5.6% in the 1st quarter, mostly due to decreased defense spending on iraq, which took .46% off the annual GDP increase rate; state & local spending & investment decreased 1.2% and knocked .14% off the gross increase…of the important private investment components, residential investment increased 19% QoQ and added .40% to the annual rate of increase, non-residential investment decreased 2.1% and subtracted .35%, and equipment & software only increased 1.7%, compared with an increase of 7.5% in the 4th quarter, as investment was pulled forward by the expiration of depreciation tax credits…bill mcbride produces an interesting chart of the investment components, included here below; what it shows is a 3 quarter average of the contributions from residential investment (red), non-residential building (blue), and equipment & software (green) to GDP, centered on the middle of the 3 quarters averaged; note that early on in the recovery, that equipment investment anchored GDP growth, but it’s now starting to lag as demand has not caught up (recall last week we noted capacity utilization fell to 78.6%)…& if you click on the chart, you should also be able to view the feint dashed line which represents increases or decreases in inventories…

for the most part, the econo-blogosphere considered this a disappointing report; especially in consideration of the 3.0% annualized growth rate seen in the 4th quarter last year; forecasters had been expecting growth between 2.5% and 2.9%, so it also surprised everyone on the downside…and some – Mish & others – complained the deflator was too small, & that real growth was even less…it’s certainly not a high enough rate of growth to bring unemployment down; economists see a relationship between GDP growth and employment they call “okun’s law”, and though its correspondence is quite inexact, it’s generally believed that it takes 3% GDP growth over a year to bring unemployment down 1%…considering that GDP growth over 2010 just barely averaged over 3%, and last year’s total growth was only 1.7%, we arent doing very well at bring those who dropped out of the labor force back in…and looking ahead, some other reports dont show much promise for the second quarter; March orders for durable goods fell by 4.2%, the largest decline in three years…and confirming the slowdown in manufacturing, all the April regional Fed indexes except Richmond indicated slowing rates of expansion…

while we’re still talking GDP growth, we ought to note that the British economy shrank in the first quarter of 2012, by 0.2%, following a 0.3% fall in their GDP in the final quarter of last year, which according to the formal definition, puts them back into a recession for a second time in this long downturn…so even after two years of conservative austerity, the confidence fairy has failed to materialize…we should also note that the UK, and most eurozone countries, report their growth as quarter over quarter, rather than at an annualized rate such as we do; so if England had reported those two quarters annualized, they’d be shown as contracting at an annual rate over 1.0%; conversely, reporting the US first quarter growth on a quarterly basis would have shown a rate of 0.5%…

this week also marked the release of the annual reports on the condition of Social Security and Medicare from the trustees for the trust funds, and as we see every year at this time, they’re greeted with typical doom from the media, ie, the funds are going bankrupt even sooner than expected….then we get the typical pushback from the blogosphere that all we have to do to “fix social security” (which implies its broken) would be to eliminate the income cap on which is it is funded (currently only income under $110,100 is taxed)…so let’s calm down & look at what we know; first, social security ran a surplus of more than $69 billion in 2011 and the trust fund increased even with this high rate of unemployment…the social security trust fund still has $2.86 trillion in US treasury bonds (here’s the list) and it can still pay full benefits until 2033, another 21 years…& at today’s low rate of payroll tax collections & life expectancy, it would still be able to pay 75% of benefits thereafter…Medicare funding is good for all needs until 2024, after which it hits a shortfall similar to social security…as Jared Bernstein, former chief economist for Joe Biden points out, the projected end date for social security full benefits has shortened 8 years entirely due to revenue shortfalls caused by the recession; it was reported fully funded till 2041 in the 2008 report…so again we’re facing a problem that virtually disappears if we get back to full employment…and coberly at angry bear further cites a CBO report that shows increasing payroll taxes just 40 cents per week each year will pay for the whole “shortfall” until 2083; obviously, the same increase in funding could be achieved by raising the minimum wage, and hence the contributions of roughly 25% of the workforce, without even increasing the payroll tax…but what’s even crazier about this entire hullaballoo is that’s predicated on economic projections 20 years and more into the future…who could have predicted today’s economic conditions even 5 years ago, in 2007?….so maybe we should just give the future a rest until it gets here…

there were a number of housing reports this week, including the february case-shiller price index…but lets start with the preliminary report on March new home sales from the census bureau, which like most reports from census, is derived from a small sampling and is subject to later revisions…the headline was that new home sales decreased 7.1% (±20.7%) in March to a seasonally adjusted annual rate of 328,000 units, but that decline resulted entirely from a revision of february’s sales to 353,000 units, now reported as an increase of 7.3% from january, which had previously been reported as a decline of 1.6% from the revised january figure…nonetheless, march sales were still 7.5% (±19.6%) above the march 2011 estimate of 305,000, so we do seem to be inching out of a trough that was unmatched in depth & severity (see graph)..the median sales price of the new houses sold was $234,500; the average sales price was $291,200…the estimated seasonally adjusted 144,000 new homes remaining on the market amounted to a 5.3 month supply at the current sale rate…the combined total of completed inventory and new homes under construction is now at the lowest level since census has kept these records….

according to the february S&P/case-shiller home price index, house prices for both of their composite indexes and nine of the 20 cities they cover hit new lows in february, with both indexes showing an 0.8% decline from the january 3 month report and annual declines of 3.6% and 3.5% for the 10- and 20-city composites, respectively…prices dropped month over month in 16 of the 20 cities the index tracks, with the worst declines being in Atlanta, Chicago and Cleveland; again, prices rose in the hard hit sun-belt cities of Phoenix, San Diego and Miami…the 10 city index is now off 34.2% from its bubble high, and the 20 city composite is off 33.9% from their home price peak…in addition to case-shiller, several other home price indexes have also reported recently; last Friday, FNC, who only reports on non-distressed residences, reported February prices were down 0.8% for the month, a seventh consecutive month-to-month decline, and 3% for the year…on the same day case shiller reported, the FHFA (Federal Housing Finance Agency) reported their price index up 0.3% for the month of February on a seasonally adjusted basis, with a 0.4% increase year over year, the first year over year gain for their index since july 2007; FHFA’s index only includes loans backed by Fannie and Freddie and it’s now 19.4% below it’s 2007 peak…RadarLogic reports an unadjusted 25 city price index based on prices paid per square foot; it showed february prices increasing 1.9% over january but down 3.19% year over year…CoreLogic reports a 3 month repeat sales index similar to case-shiller, but weighted heavier for recent months; they also showed February home prices to have declined by 0.8 percent compared to January, the seventh consecutive monthly decline; they report a 2.0% year-over-year decline for their february index…excluding distressed sales, their month-over-month prices increased 0.7% in february from january, with a year over year decline of only 0.8%…others are getting into the home price reporting as well…according to the NAR (realtors) the median sales price of an existing home increased to $163,800 in March from $155,600 in February…& trulia initiated a home asking price index this month, which showed asking prices in march were up 0.9% after rising 0.6% in february…whether it’s spring fever or what, there were more optimistic home price forecasts this week than i’ve seen all year; everyone is saying prices have bottomed and its time to buy; even the normally reserved bill mcbride got on the bandwagon…but we’d be wise to heed economist Robert Shiller, who’s probably studied home price trends more than anyone, & who believes there will be no housing rebound for a generation…

RealtyTrac was out with it’s first quarter report on foreclosure activity, which showed it had increased in 26 of the 50 large metro areas they reported on, with Pittsburgh showing the largest increase at 49 percent; generally, foreclosure activity was up in states with a foreclosure judicial process, & down in states where court action is unnecessary for banks to repossess a home…LPS (Lender Processing Services) was also out with their “First Look” for March, which gives preliminary details on delinquent mortgage loans and homes currently in foreclosure; LPS reported the mortgage delinquency rate declined to 7.09% from 7.57% in February, which was the lowest delinquency rate since August of 2008; they also reported 2,060,000 homes in the foreclosure process, representing 4.15% of all homes with mortgages, a number only slightly down from the 2,222,000 in foreclosure last year at this time…a separate report from LPS showed short sales (wherein the homeowner sells the house on behalf of the bank for less than the mortgage) accounted for 23.9% of January home sales, compared with 19.7% for foreclosures, which was a 33% increase in short sales over a year ago; the bank servicers are encouraging short sales in lieu of foreclosure because they usually sell for more, the banks dont get saddled with upkeep of foreclosed properties, and by negotiating such a deal with the homeowner, they dont have to produce the paperwork to prove their right to foreclose in court…

(the above is my weekly commentary that accompanied my sunday morning links mailing, which in turn was mostly selected from my weekly blog post on the global glass onion, and also includes other links of interest…if you’d be interested in getting my weekly emailing of selected links that accompanies these commentaries, most coming from the aforementioned GGO posts, contact me…)

{kind=link}

{kind=link}

{kind=link}